years

$XX,XX5

Copied!

Share

Copy link

Twitter

Facebook

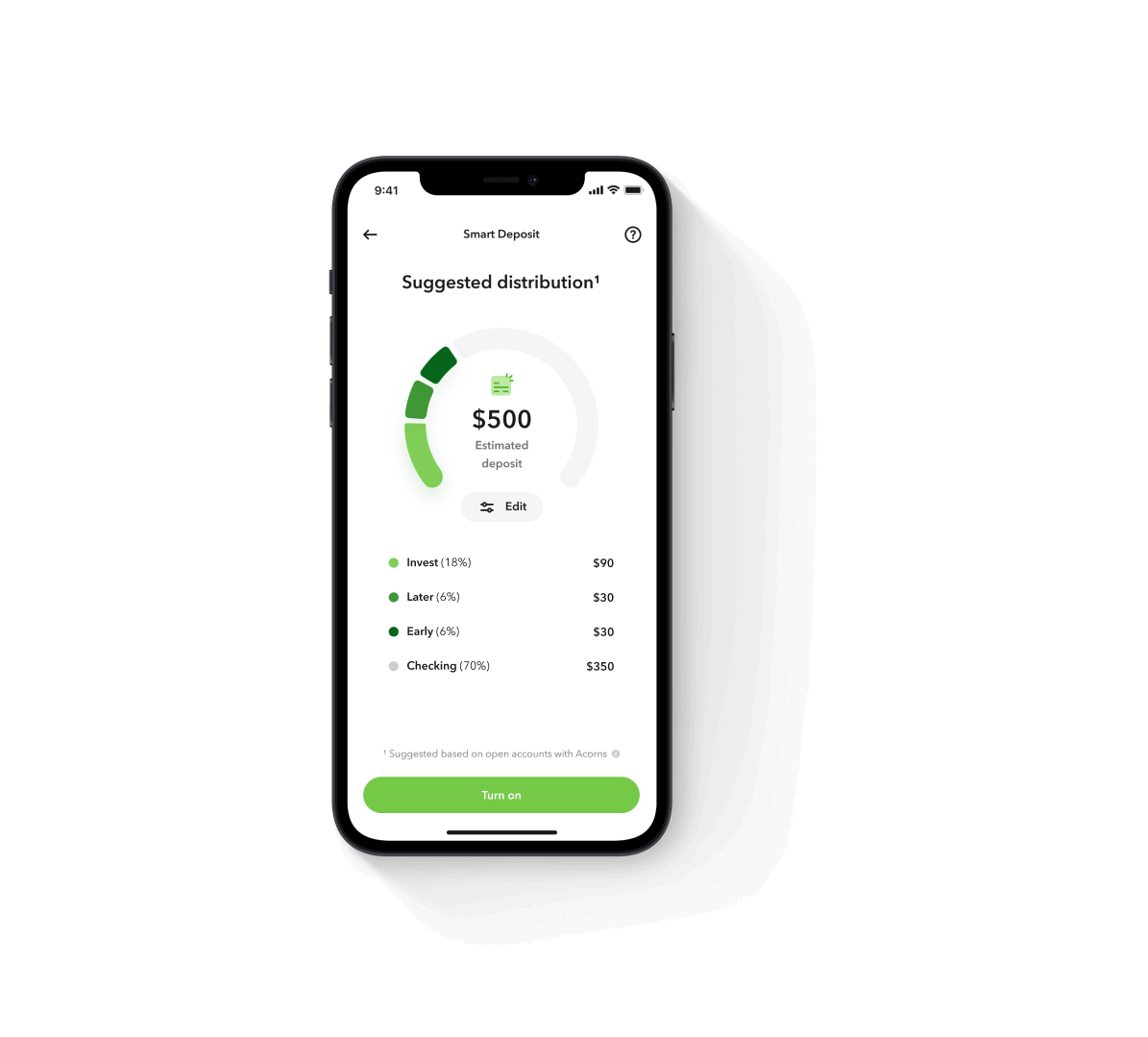

The chart shows an estimate of how much an investment could grow over time based on the initial deposit, contribution schedule, time horizon, and interest rate specified. Changes in those variables can affect the outcome. Reset the calculator using different figures to show different scenarios. Results do not predict the investment performance of any Acorns portfolio and do not take into consideration economic or market factors which can impact performance.